import pandas as pd

import numpy as np

import matplotlib. pyplot as plt

from sklearn. preprocessing import MinMaxScaler

from keras. models import Sequential

from keras. layers import Dense, LSTM, Dropout

from keras. optimizers import SGD

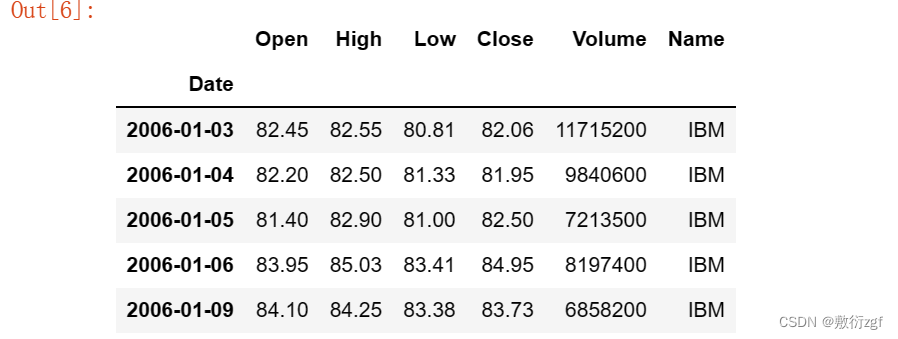

dataset = pd. read_csv( "datasets_8388_11883_IBM_2006-01-01_to_2018-01-01.csv" , index_col= 'Date' , parse_dates= [ 'Date' ] )

dataset. head( )

dataset. shape

train_set = dataset[ : '2016' ] . iloc[ : , 1 : 2 ] . values

test_set = dataset[ '2017' : ] . iloc[ : , 1 : 2 ] . values

train_set. shape

test_set. shape

def plot_predictions ( test_result, predict_result) :

"""

test_result:真实值

predict_result: 预测值

"""

plt. plot( test_result, color= 'red' , label= 'IBM True Stock Price' )

plt. plot( predict_result, color= 'blue' , label= 'IBM Predicted Stock Price' )

plt. title( 'IBM Stock Price' )

plt. xlabel( 'Time' )

plt. ylabel( 'Stock Price' )

plt. legend( )

plt. show( )

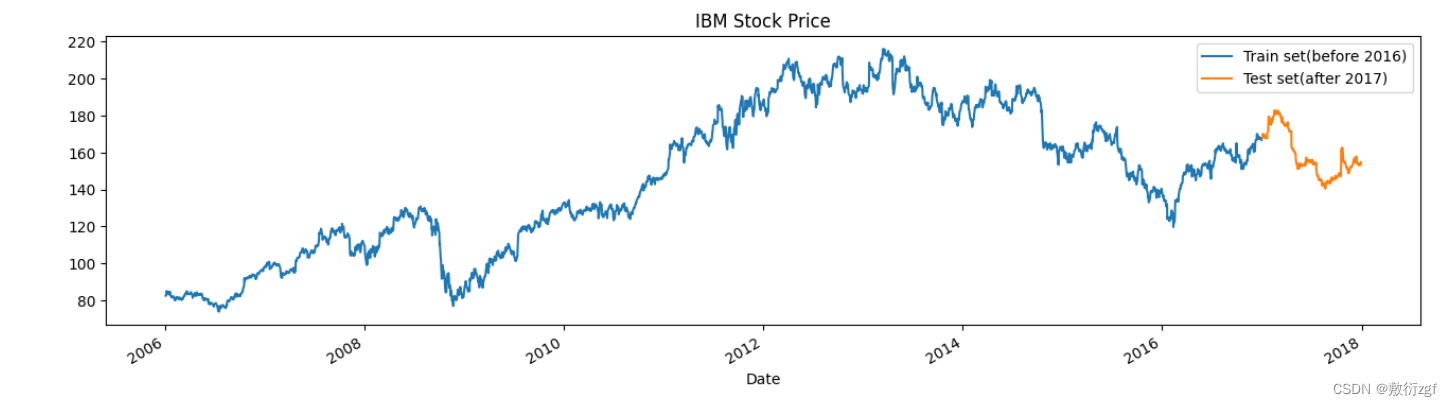

dataset[ 'High' ] [ : '2016' ] . plot( figsize= ( 16 , 4 ) , legend= True )

dataset[ 'High' ] [ '2017' : ] . plot( figsize= ( 16 , 4 ) , legend= True )

plt. title( 'IBM Stock Price' )

plt. legend( [ 'Train set(before 2016)' , 'Test set(after 2017)' ] )

plt. show( )

sc = MinMaxScaler( feature_range = [ 0 , 1 ] )

train_set_scaled = sc. fit_transform( train_set)

X_train = [ ]

y_train = [ ]

for i in range ( 60 , 2769 ) :

X_train. append( train_set_scaled[ i- 60 : i, 0 ] )

y_train. append( train_set_scaled[ i, 0 ] )

X_train, y_train = np. array( X_train) , np. array( y_train)

X_train. shape

X_train[ 0 ]

X_train = np. reshape( X_train, ( X_train. shape[ 0 ] , X_train. shape[ 1 ] , 1 ) )

X_train. shape

model = Sequential( )

model. add( LSTM( 128 , return_sequences= True , input_shape= ( X_train. shape[ 1 ] , 1 ) ) )

model. add( Dropout( 0.2 ) )

model. add( LSTM( 128 , return_sequences= True ) )

model. add( Dropout( 0.2 ) )

model. add( LSTM( 128 ) )

model. add( Dropout( 0.2 ) )

model. add( Dense( units= 1 ) )

model. compile ( optimizer= 'rmsprop' , loss= 'mse' )

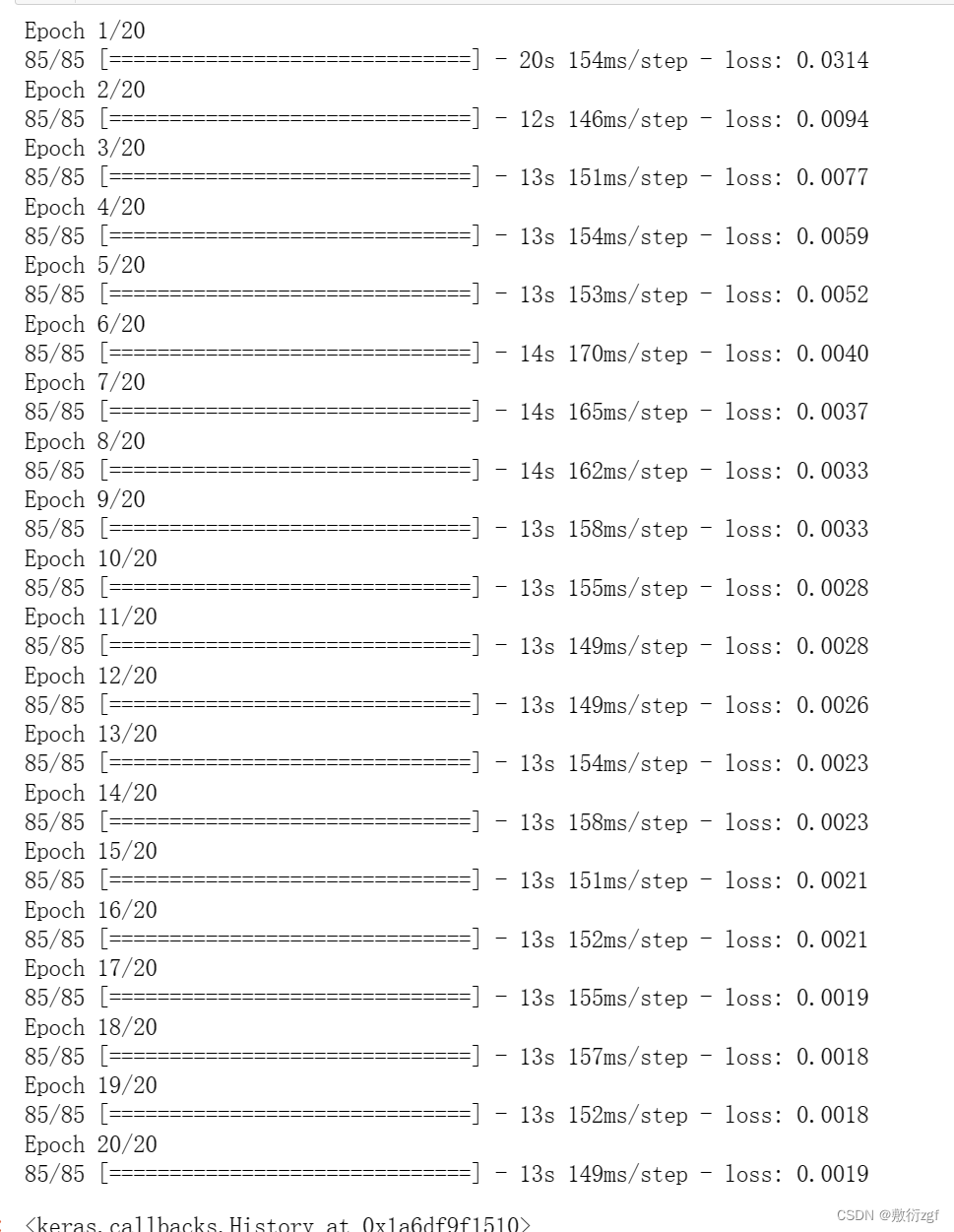

model. fit( X_train, y_train, epochs= 20 , batch_size= 32 )

dataset_total = pd. concat( ( dataset[ 'High' ] [ : '2016' ] , dataset[ 'High' ] [ '2017' : ] ) , axis = 0 )

dataset_total. shape

dataset_total

inputs = dataset_total[ len ( train_set) : ] . values

inputs = inputs. reshape( - 1 , 1 )

inputs. shape

inputs_scaled = sc. fit_transform( inputs)

dataset_total = pd. concat( ( dataset[ 'High' ] [ : '2016' ] , dataset[ 'High' ] [ '2017' : ] ) , axis= 0 )

inputs = dataset_total[ len ( dataset_total) - len ( test_set) - 60 : ] . values

inputs

inputs = inputs. reshape( - 1 , 1 )

inputs = sc. transform( inputs)

inputs. shape

X_test = [ ]

for i in range ( 60 , 311 ) :

X_test. append( inputs[ i- 60 : i, 0 ] )

X_test = np. array( X_test)

X_test. shape

X_test = np. reshape( X_test, ( X_test. shape[ 0 ] , X_test. shape[ 1 ] , 1 ) )

X_test. shape

predict_test = model. predict( X_test)

predict_test. shape

predict_stock_price = sc. inverse_transform( predict_test)

predict_stock_price

plot_predictions( test_set, predict_stock_price)